A practical reference for founders, investors, CFOs, shareholders and tax professionals

If you have ever tried to price a share in a private company, you already know the problem. A listed company’s share has a price you can check in seconds. A private company’s share does not. There is no ticker, no daily quote, nothing to point to.

That is exactly the gap Rule 11UA was built to close. It gives every unlisted company, every investor, and every tax officer in India one common method to work out what an unquoted share is actually worth for tax purposes.

At BBMCo, questions about Rule 11UA come up constantly, from founders preparing a funding round, from families transferring shares during succession planning, and from investors trying to understand their capital gains exposure.

This guide answers those questions in one place, in plain language, based on the law as it stands in 2026.

What is Rule 11UA?

| Quick Answer Rule 11UA of the Income Tax Rules, 1962 is the provision that prescribes how to calculate the Fair Market Value (FMV) of unquoted shares, securities, jewellery and artistic work for Indian income tax purposes. It applies whenever a transaction has no observable market price, and it is the value that other sections, such as Section 50CA and the gift taxation provision, rely on to test whether a transaction was priced fairly. |

In simple terms, Rule 11UA is the rulebook the tax department uses to check whether a private company’s shares were bought, sold, gifted, or issued at a reasonable price.

If your transaction price does not match the Rule 11UA value closely enough, you could end up paying tax on a value you never actually received, or a value you never actually paid.

The rule sits under Section 56 of the Income-tax Act, 1961, carried forward as Section 92 of the Income-tax Act, 2025 effective from Tax Year 2026-27.

But its influence stretches well beyond gift taxation alone, reaching into capital gains, ESOP taxation, and company law valuation requirements as well.

Why Was Rule 11UA Introduced?

Before Rule 11UA existed in its current form, there was no consistent way to value an unlisted company’s shares for tax purposes.

Two parties could agree on almost any price they wanted, and the tax department had limited grounds to challenge it.

That created an obvious loophole. A shareholder could sell shares worth crores for a token amount to a related party, avoiding capital gains tax almost entirely.

A closely held company could receive share premiums far above real value from investors, effectively routing unaccounted money into the business through inflated share capital.

Rule 11UA was designed to remove that discretion. By prescribing a fixed formula for equity shares and a documented open-market approach for other securities, it gives both taxpayers and tax officers a shared, auditable starting point.

Disagreements can still happen, but they now happen over specific balance sheet numbers rather than an arbitrary opinion of value.

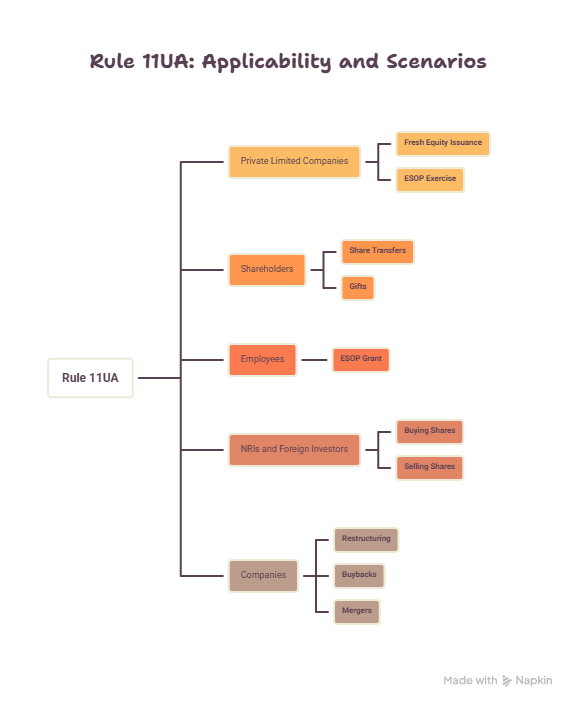

Who Does Rule 11UA Apply To?

Rule 11UA applies to anyone dealing with unquoted shares or securities of an Indian company where a tax question depends on fair value. In practice, this covers:

• Private limited companies issuing fresh equity shares to investors

• Shareholders transferring shares in an unlisted company, including within families

• Individuals or entities receiving shares as a gift or for less than fair value

• Employees exercising ESOPs granted by a private company

• NRIs and foreign investors buying or selling shares in Indian unlisted companies

• Companies undergoing restructuring, buybacks, or mergers involving unquoted shares

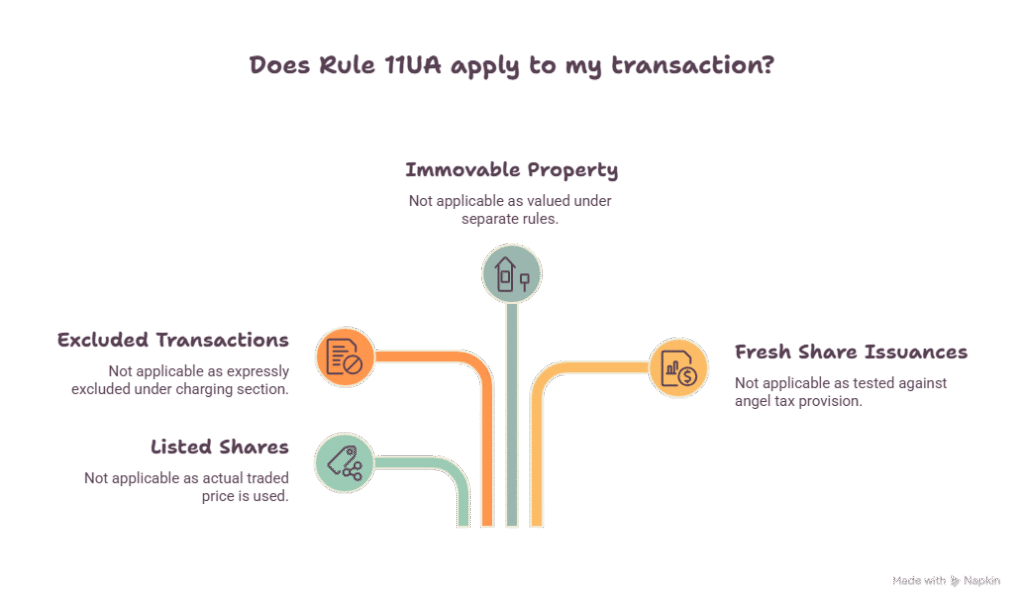

Who Does It Not Apply To?

Rule 11UA does not apply to:

- Shares of listed companies traded through a recognised stock exchange, where the actual traded price is used instead of a formula.

- Transactions expressly excluded under the relevant charging section, such as certain classes of persons carved out under Section 50CA.

- Immovable property considered on its own, which is valued under separate rules, though stamp duty value does feed into the Rule 11UA formula as one component.

- Fresh share issuances tested only against the erstwhile angel tax provision, since Section 56(2)(viib) no longer applies from Assessment Year 2025-26 onward.

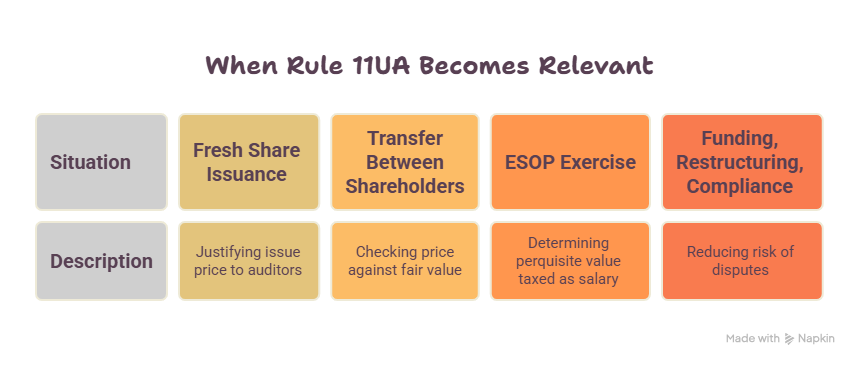

When Does Rule 11UA Become Relevant?

Rule 11UA becomes relevant at the exact moment a transaction involving unquoted shares needs a tax value assigned to it. Four situations come up most often in practice:

1. A Fresh Share Issuance

When a private company issues new shares, it often needs to justify the issue price to auditors, incoming investors, or in response to a tax query for an earlier year.

2. A Transfer Between Shareholders

When shares change hands by sale, gift, or family transfer, the actual price needs to be checked against fair value under Section 50CA and the gift taxation provision.

3. An ESOP Exercise

When an employee exercises stock options in a private company, the perquisite value taxed as salary depends on the FMV on the exercise date.

4. Funding, Restructuring, or Statutory Compliance

When a company prepares for external funding, an internal restructuring, or statutory disclosure under the Companies Act, a defensible valuation report reduces the risk of disputes later.

Meaning of Fair Market Value (FMV)

Fair Market Value is the price an asset would fetch if sold in the open market between a willing buyer and a willing seller, with both parties acting without pressure and with reasonable knowledge of the relevant facts.

For listed shares, FMV is easy to establish. It is simply the quoted market price. For unlisted shares, there is no market price to observe, which is exactly why Rule 11UA exists: to build a defensible, formula-based substitute for that missing market price.

How FMV Is Calculated Under Rule 11UA

Rule 11UA(1) sets out four separate categories of property, each with its own valuation approach.

| Category | Valuation Approach |

| Jewellery | Open market price on the valuation date; invoice value if purchased from a registered dealer; registered valuer’s report required if value exceeds Rs 50,000 and it was received other than by purchase |

| Artistic work (paintings, sculptures, archaeological collections) | Same three-tier approach as jewellery |

| Quoted shares and securities | Recorded stock exchange transaction value, or the lowest quoted price on the valuation date, or the last trading day before it if there was no trading on the valuation date |

| Unquoted equity shares | NAV-based formula under Rule 11UA(1)(c)(b) |

| Unquoted shares/securities other than equity (preference shares, debentures) | Open market price, supported by a merchant banker or accountant report, under Rule 11UA(1)(c)(c) |

The category that generates the most compliance activity, by far, is unquoted equity shares. That is where the well-known Rule 11UA formula comes in.

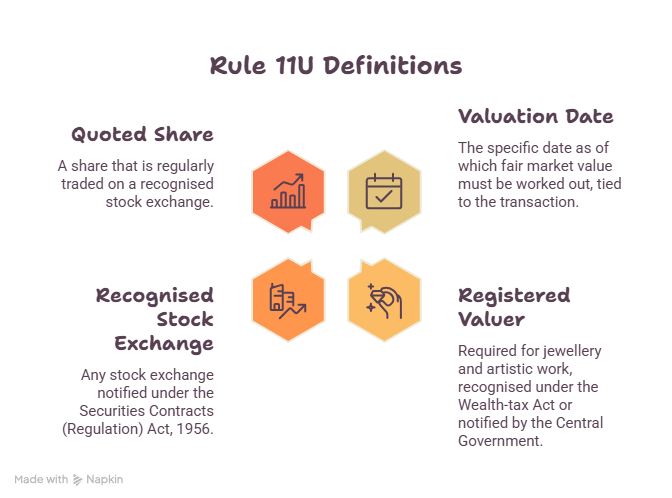

Rule 11U: The Definitions Behind Rule 11UA

Rule 11UA does not stand alone. It depends on a set of definitions laid out in the preceding rule, Rule 11U, and understanding two or three of these terms clears up most of the confusion people have about how the formula actually applies.

Valuation Date

The valuation date is the specific date as of which fair market value must be worked out. It is not a fixed date each year.

It is tied to the transaction itself, generally the date of the gift, the date of transfer, or the date shares are issued or subscribed, depending on which section is being applied.

Registered Valuer

For jewellery and artistic work, Rule 11U requires a registered valuer as recognised under the Wealth-tax Act framework carried into these rules, or as notified by the Central Government.

This is distinct from a merchant banker or a chartered accountant, who handle share and security valuations instead.

Recognised Stock Exchange and Quoted Share

Rule 11U defines a recognised stock exchange as any stock exchange notified under the Securities Contracts (Regulation) Act, 1956. A share only qualifies as “quoted” if it is regularly traded on such an exchange.

A share that is technically listed but rarely traded may still need to be valued as an unquoted share in practice, since Rule 11UA(1)(c)(a) depends on there being an actual, current trading price to reference.

Keeping these definitions in mind matters because a valuation report that gets the valuation date wrong, or that treats a thinly traded listed share as freely quoted, can be challenged on that basis alone, regardless of how correctly the rest of the formula was applied.

Rule 11UA Formula Explained

For unquoted equity shares, Rule 11UA(1)(c)(b) prescribes the following formula:

| The Rule 11UA FormulaFMV = (A + B + C + D − L) × (PV / PE) |

Here is what each variable in the formula stands for:

| Variable | Meaning |

| A | Book value of all assets other than jewellery, artistic work, shares, securities and immovable property, adjusted for income tax paid (net of refunds) and unreal assets such as unamortised deferred expenditure |

| B | Open market value of jewellery and artistic work, based on a registered valuer’s report |

| C | Fair market value of shares and securities held by the company, valued under this same rule |

| D | Stamp duty value of any immovable property held by the company |

| L | Book value of liabilities, excluding paid-up equity capital, undeclared dividends, reserves and surplus, excess tax provisions, and most contingent liabilities |

| PV | Paid-up value of the equity share being valued |

| PE | Total paid-up equity share capital shown in the balance sheet |

Read plainly, the formula takes the company’s real net worth (assets minus liabilities, adjusted for a few specific items) and divides it proportionally across the paid-up equity capital. What comes out the other end is a defensible, per-share net asset value.

A Simple Worked Example

Assume a private company, Nimbus Textiles Private Limited, is valuing its shares as of a chosen valuation date.

| Item | Amount |

| Total adjusted assets (A + B + C + D) | Rs 6,00,00,000 |

| Total liabilities (L) | Rs 1,50,00,000 |

| Paid-up equity capital (PE) | Rs 50,00,000 (5,00,000 shares of Rs 10 each) |

| Face value per share (PV) | Rs 10 |

Step 1: Net value = Rs 6,00,00,000 − Rs 1,50,00,000 = Rs 4,50,00,000

Step 2: FMV per share = Rs 4,50,00,000 × (Rs 10 / Rs 50,00,000) = Rs 90 per share

A share with a face value of Rs 10 carries a Rule 11UA fair market value of Rs 90.

If shares in this company are transferred at a price well below Rs 90, it can trigger tax exposure under Section 50CA for the seller and under the gift taxation provision for the buyer, depending on the size of the shortfall.

The NAV Method

The Net Asset Value method is the approach built directly into Rule 11UA’s formula.

It values a company based on what it owns today, adjusted for what it owes, rather than what it might earn in the future.

NAV works well for established, asset-heavy businesses such as manufacturing units, real estate holding companies, or trading firms with a stable balance sheet.

It is less suited to a business whose real value lies in future growth rather than current assets.

The DCF Method

The Discounted Cash Flow method values a company based on its projected future cash flows, discounted back to today’s value.

For many years, it was the preferred method for startups issuing shares at a premium to justify valuations well above their current net worth.

Under the Income Tax Rules, the DCF method for unquoted equity shares appears specifically in Rule 11UA(2), which was framed to test share premiums under the erstwhile angel tax provision, Section 56(2)(viib).

Since that provision no longer applies to fresh share issuances from Assessment Year 2025-26 onward, DCF’s role under Rule 11UA has narrowed considerably, and it now mainly applies to assessments for earlier years that are still pending.

Valuation of Compulsorily Convertible Preference Shares (CCPS)

CCPS are common in startup funding rounds, since investors often prefer preference shares that convert into equity later rather than subscribing to equity directly.

Rule 11UA(2)(B) addresses this specifically, for the purposes of the erstwhile angel tax provision.

Under this clause, the fair market value of CCPS can be determined either using the same methods available for unquoted equity shares (NAV, DCF, VC benchmarking, or the additional non-resident methods), or based on the FMV of the equity shares the CCPS will eventually convert into, at the option of the assessee.

As with the rest of Rule 11UA(2), this clause’s practical relevance today is mostly confined to legacy assessments from before Assessment Year 2025-26. For fresh CCPS issuances now, the more relevant question is usually Section 50CA on a later transfer or conversion, rather than angel tax on issuance.

NAV vs DCF: A Quick Comparison

| Factor | NAV Method | DCF Method |

| Basis of valuation | Current balance sheet (assets minus liabilities) | Projected future cash flows |

| Best suited for | Asset-heavy, established businesses | High-growth or early-stage businesses |

| Who can certify it | Computed directly from audited financials | Must be certified by a SEBI-registered merchant banker |

| Current relevance under Rule 11UA | Applies broadly: gifts, Section 50CA transfers, ESOP exercises | Mainly relevant to legacy angel tax assessments from before AY 2025-26 |

| Degree of subjectivity | Low; formula driven | Higher; depends on growth assumptions |

Merchant Banker vs Chartered Accountant: Who Should You Engage?

| Aspect | Merchant Banker | Chartered Accountant |

| Certify DCF valuation under Rule 11UA(2) | Yes, mandatory for this purpose | Not for DCF specifically |

| Certify FMV of non-equity unquoted securities under Rule 11UA(1)(c)(c) | Yes | Yes, permitted as an alternative |

| Regulatory oversight | SEBI-registered | ICAI-regulated |

| Typical engagement | Larger fundraising rounds, formal DCF certifications | NAV computations, smaller transactions, general compliance valuations |

For a straightforward NAV valuation drawn from an audited balance sheet, a chartered accountant is generally the right professional to engage.

Certain valuations, particularly DCF-based share premium justifications, require a SEBI-registered merchant banker by law.

Rule 11UA and Startup Funding

For years, one of the first questions a founder asked before a funding round was which Rule 11UA method to use, since the wrong choice could mean the difference between a smooth fundraise and a tax notice.

Founders should still prepare a defensible valuation for any share issuance, but the reason has shifted. It is no longer primarily about avoiding an angel tax demand, since that provision no longer applies to new issuances.

Instead, a solid valuation record protects the company if a Section 50CA question arises later on a share transfer, supports due diligence during the next funding round, and satisfies Companies Act disclosure requirements around share issue pricing.

Rule 11UA After the Abolition of Angel Tax

The Finance Act, 2024 removed Section 56(2)(viib), commonly known as angel tax, with effect from Assessment Year 2025-26.

This is one of the most significant recent changes affecting Rule 11UA, and also one of the most misunderstood.

Angel tax used to be the primary reason startups engaged closely with Rule 11UA(2) to (4): the sub-rules that offered multiple valuation routes, including DCF certified by a merchant banker, benchmarking against a recent venture capital round within a 90-day window, and five additional methods reserved for non-resident investors, along with a 10 percent safe harbour variance between issue price and computed value.

With angel tax gone for fresh issuances, these expanded sub-rules have lost their main trigger. They remain relevant only where an assessment for a year before AY 2025-26 is still open or under dispute.

| What Has Not Changed Rule 11UA(1), including the core NAV formula for unquoted equity shares and the open-market approach for other unquoted securities, continues to remain relevant wherever the applicable income tax provisions require the determination of fair market value, including transactions covered by Section 50CA and the provisions relating to taxation of certain gifts. Although the angel tax provisions have been abolished, Rule 11UA continues to play an important role in determining the fair market value of unlisted shares and other specified assets wherever the law requires such a valuation. |

Rule 11UA Under the Income-tax Act, 2025

The Income-tax Act, 2025 took effect from 1 April 2026, alongside the Income-tax Rules, 2026, replacing the 1961 Act and 1962 Rules for Tax Year 2026-27 onward.

For returns filed in July 2026 covering FY 2025-26 (Assessment Year 2026-27), taxpayers continue to use the old section numbers under the 1961 Act.

The renumbered provisions, including Section 92 in place of Section 56, apply only from Tax Year 2026-27 returns filed from July 2027 onward.

The valuation principles governing the determination of the fair market value of unquoted shares continue under the Income-tax Act, 2025 and the Income-tax Rules, 2026. However, references, section numbers, and drafting have been reorganised as part of the new legislative framework.

Businesses involved in transactions during the transition period should ensure that valuation reports and supporting documentation refer to the correct legal provisions applicable to the relevant tax year.

What Changed After 1 April 2026?

| Before 1 April 2026 | From 1 April 2026 |

| Income-tax Act, 1961 | Income-tax Act, 2025 |

| Income-tax Rules, 1962 | Income-tax Rules, 2026 |

| Previous Year / Assessment Year terminology | Tax Year terminology introduced under the new Act |

| Old section references | Renumbered provisions under the new Act |

| Valuation principles under Rule 11UA | Continue under the new legislative framework with updated references where applicable |

Note: During the transition period, taxpayers should ensure they apply the correct law and section references based on the relevant tax year.

Rule 11UA vs Rule 11UAA: What Is the Difference?

Rule 11UA and Rule 11UAA are frequently confused because they deal with adjacent valuation questions.

| Rule 11UA | Rule 11UAA | |

| Applies to | Jewellery, art, quoted shares, and unquoted equity shares and securities | Unquoted shares other than equity shares, specifically for Section 50CA |

| Governing purpose | FMV for gift taxation and as the base method for Section 50CA equity transfers | FMV for Section 50CA transfers of non-equity unquoted shares |

| Method for equity shares | NAV formula: (A+B+C+D−L) × PV/PE | Cross-refers to Rule 11UA(1)(c)(b)/(c) |

| Valuer required | Registered valuer for jewellery/art; merchant banker or accountant optional for other securities | Merchant banker or accountant report |

In short, Rule 11UAA does not replace Rule 11UA. It borrows Rule 11UA’s methodology and applies it specifically to capital gains on the transfer of non-equity unquoted instruments, such as preference shares and CCPS.

Rule 11UA vs Rule 11UB: Don’t Confuse the Two

Rule 11UB is a different provision entirely, and the similar numbering causes genuine confusion.

Rule 11UB prescribes how to value the assets of an Indian company or entity for the purposes of Section 9(1)(i), which deals with indirect transfer of Indian assets by a foreign entity, and it also intersects with slump sale valuation requirements under Section 50B.

Rule 11UA values shares and securities directly. Rule 11UB values the underlying business assets of a company, primarily in cross-border indirect transfer and slump sale contexts.

If your transaction is a straightforward share purchase, sale, gift, or issuance, Rule 11UA is the relevant provision.

Rule 11UB becomes relevant only in specific slump sale and indirect transfer scenarios, which most domestic share transactions never touch.

Rule 11UA vs FEMA Pricing Guidelines: A Common Point of Confusion

Founders raising money from foreign investors often assume that a Rule 11UA valuation automatically satisfies every regulatory requirement around the transaction.

It does not. Rule 11UA is an income tax valuation, governed by the CBDT. Foreign investment into an Indian company is separately governed by FEMA pricing guidelines, administered by the RBI, which apply whenever shares are issued to or transferred from a non-resident.

FEMA pricing guidelines require that shares issued to a non-resident be priced at or above fair value, determined under an internationally accepted pricing methodology, certified by a merchant banker or a chartered accountant.

On a share transfer from a resident to a non-resident, the price cannot exceed fair value; on a transfer from a non-resident to a resident, it cannot be below fair value.

| Why this distinction matters A single valuation report can often be structured to satisfy both requirements at once, but the two frameworks exist for different reasons, answer to different regulators, and are not automatically interchangeable. A transaction involving foreign investment should be checked against both Rule 11UA and FEMA pricing guidelines before it closes, not just one or the other. |

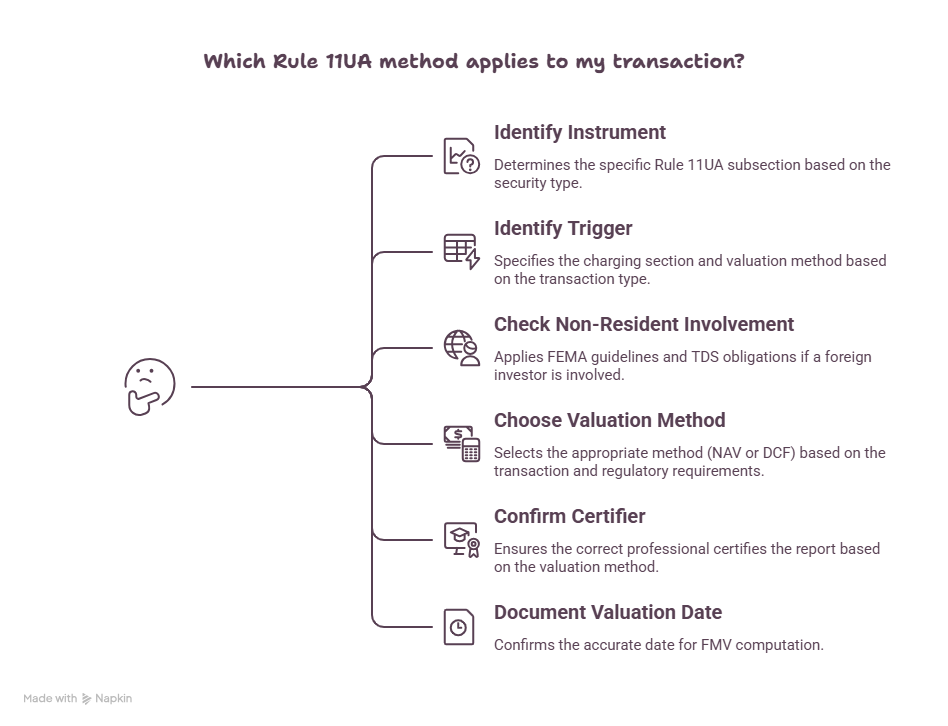

Decision Framework: Which Rule 11UA Method Applies to You?

Use this sequence to work out which part of Rule 11UA is actually relevant to your transaction, before engaging a valuer.

- Identify the instrument: Is it equity shares, preference shares (including CCPS), or another security like a debenture? Equity goes to Rule 11UA(1)(c)(b). Everything else generally goes to Rule 11UA(1)(c)(c), or Rule 11UAA if the context is a Section 50CA transfer.

- Identify the trigger: Is this a fresh issuance, a transfer between existing holders, a gift, an ESOP exercise, or a buyback? This determines which charging section, Section 50CA or the gift taxation provision, will actually use the FMV you calculate.

- Check if a non-resident is involved: If a foreign investor or NRI is on either side of the transaction, FEMA pricing guidelines apply in addition to Rule 11UA, and TDS obligations under Section 195 may also come into play.

- Choose the appropriate valuation method: The NAV method is commonly used for many share transfers, gifts, and other transactions where it is prescribed under the applicable valuation provisions. The DCF method continues to be widely used for startup fundraising, FEMA pricing, commercial valuations, and investment decisions. Following the abolition of the angel tax provisions, its use under the former Section 56(2)(viib) framework has reduced, but DCF remains an important valuation methodology in many commercial and regulatory situations.

- Confirm who needs to certify the report. A chartered accountant is generally sufficient for NAV computations. A SEBI-registered merchant banker is legally required wherever DCF certification under Rule 11UA(2) is being used.

- Document the valuation date correctly. Confirm the exact date the FMV should be computed as of, per Rule 11U, before finalising the report.

What Courts Have Said: Key Judicial Precedents

Rule 11UA has generated a substantial body of case law, mostly around whether an Assessing Officer can reject a taxpayer’s chosen valuation method.

A few decisions are worth knowing, since they shape how much room the tax department actually has to challenge a valuation report.

Vodafone M-Pesa Ltd. v. PCIT (Bombay High Court, 2018)

The Bombay High Court held that the choice between the NAV method and the DCF method under Rule 11UA belongs to the assessee, not the Assessing Officer.

The AO can scrutinise the valuation report and challenge specific assumptions, but cannot unilaterally switch the method the taxpayer selected.

Cinestaan Entertainment Pvt. Ltd. v. ITO (Delhi High Court, 2021)

The Delhi High Court upheld a startup’s DCF valuation and rejected the tax department’s argument that the valuation was invalid simply because actual results later diverged from the projections used.

The court confirmed that both NAV and DCF are recognised, and that valuation is inherently forward-looking and not meant to be judged with hindsight.

PCIT v. A.H. Multisoft Pvt. Ltd. (Delhi High Court, 2025)

More recently, the Delhi High Court reaffirmed the same principle: a DCF valuation certified by a qualified merchant banker cannot be arbitrarily replaced with an NAV valuation unless the underlying assumptions are shown to be patently erroneous or made in bad faith.

| The common thread Across these rulings, the consistent message is that a properly certified valuation report, prepared in good faith and grounded in the information available on the valuation date, is difficult for the tax department to overturn merely because hindsight tells a different story. This is precisely why documentation quality matters more than the specific method chosen. |

Penalties and Risks of Getting the Valuation Wrong

The immediate consequence of an incorrect or indefensible Rule 11UA valuation is usually a tax addition, either under Section 50CA on the seller’s side or the gift taxation provision on the recipient’s side. But the exposure does not stop there:

• Misreporting penalty under Section 270A, which can reach 200 percent of the tax payable on the under-reported income where the tax department treats the valuation gap as misreporting rather than a bona fide estimate

• Reassessment risk under Section 148, which allows the department to reopen an assessment for past years, in some cases going back up to ten years, where income is considered to have escaped assessment

• Interest on the additional tax demand from the original due date, which accrues regardless of how the dispute is eventually resolved

• Downstream complications in due diligence for a future funding round or exit, if an earlier valuation is later challenged or found indefensible

None of this means every valuation needs to be defended in court. In practice, a well-documented report prepared by a qualified professional, using reasonable and disclosed assumptions, resolves the overwhelming majority of queries at the assessment stage itself, long before litigation becomes a possibility.

Common Mistakes Businesses Make

- Using an outdated balance sheet instead of the figures as of the correct valuation date.

- Forgetting to value subsidiary shareholdings (component C) using the same Rule 11UA formula, cascading through each layer of holding.

- Valuing immovable property at book value instead of the stamp duty value the rule specifically requires (component D).

- Assuming DCF and VC-benchmarking routes under Rule 11UA(2) are still available for a current-year share issuance, when they now apply mainly to open assessments from before AY 2025-26.

- Misclassifying Ind AS fair value adjustments, which can distort the liabilities figure if not corrected.

- Skipping a formal valuation report for smaller transactions on the assumption that scrutiny is unlikely, leaving nothing to show if a notice does arrive.

Checklist Before Obtaining a Valuation Report

- Confirm the correct valuation date for the transaction.

- Gather the latest audited balance sheet as of that date.

- Identify whether the shares involved are equity or non-equity (preference shares, CCPS, debentures).

- Check whether the transaction calls for the NAV method, the DCF method, or the open-market approach.

- Confirm whether a merchant banker certification is legally required for the chosen method.

- List any subsidiary shareholdings that need their own Rule 11UA valuation.Identify any immovable property held by the company and confirm its stamp duty value.

- Decide which provision the valuation needs to support: Section 50CA, gift taxation, ESOP perquisite, or Companies Act compliance.

Real World Practical Examples

Example 1: A family share transfer

A father transfers shares in the family’s private manufacturing business to his son as part of succession planning, at a price below Rule 11UA fair value.

Transfers between specified relatives are generally exempt from gift taxation, but the family should still document the Rule 11UA valuation.

It supports the transaction if the shares change hands again later and establishes a clean cost basis for future capital gains computation.

Example 2: An ESOP exercise

An employee at a private technology company exercises stock options after the company’s last funding round priced shares well above the original grant price.

The perquisite value taxed as salary income is based on the Rule 11UA fair market value on the exercise date, not the price the employee actually paid, which makes a current valuation report essential at the time of exercise.

Example 3: A buyback from a departing shareholder

A departing co-founder sells shares back to the company at a negotiated price. If that price is lower than the Rule 11UA fair value, Section 50CA can substitute the FMV as the deemed sale consideration for the departing shareholder’s capital gains computation, regardless of what was actually paid.

Frequently Asked Questions

What is Rule 11UA in simple terms?

Rule 11UA is the Income Tax Rule that explains how to work out the fair value of shares in a private company, since there is no stock exchange price to rely on.

Is Rule 11UA valuation mandatory for every private company?

It is not mandatory for every company at every point in time, but it becomes necessary whenever a transaction, such as a share issue, transfer, gift, or ESOP exercise, needs to be tested against fair value for tax purposes.

What is the Rule 11UA formula?

FMV = (A + B + C + D − L) × (PV / PE), where the variables represent adjusted assets, liabilities, and paid-up capital, as detailed earlier in this guide.

Who can prepare a Rule 11UA valuation report?

For NAV-based valuations, a chartered accountant working from the audited balance sheet is generally sufficient. DCF valuations under Rule 11UA(2) require certification by a SEBI-registered merchant banker.

Does Rule 11UA still matter after angel tax was abolished?

Yes. Angel tax under Section 56(2)(viib) no longer applies to fresh share issuances from Assessment Year 2025-26, but Rule 11UA’s core valuation methods still apply to gift taxation and capital gains under Section 50CA.

What is the difference between Rule 11UA and Rule 11UAA?

Rule 11UA covers jewellery, artistic work, quoted shares, and unquoted equity shares. Rule 11UAA specifically addresses non-equity unquoted shares, such as preference shares, for the purposes of Section 50CA, and largely borrows Rule 11UA’s methodology.

What happens if shares are sold below Rule 11UA fair value?

The seller can be taxed under Section 50CA on the FMV instead of the actual sale price, and the buyer can be taxed under the gift taxation provision if the shortfall exceeds Rs 50,000.

Does Rule 11UA apply to NRIs?

Yes. NRIs buying or selling shares in Indian unlisted companies are subject to the same Rule 11UA valuation requirements, along with associated TDS obligations.

How often should a company update its Rule 11UA valuation?

A fresh valuation is generally needed for each transaction event, such as a new share issue, transfer, or ESOP exercise, since FMV is tied to a specific valuation date rather than a fixed annual figure.

Will Rule 11UA change under the Income-tax Act, 2025?

The section numbers that reference Rule 11UA are changing as part of the broader renumbering exercise, but the substance of the valuation methodology is expected to continue without material change.

Key Takeaways

• Rule 11UA sets the method for valuing unquoted shares, securities, jewellery and artistic work for Indian income tax purposes.

• The NAV formula, FMV = (A+B+C+D−L) × (PV/PE), is the standard method for unquoted equity shares.

• Non-equity unquoted securities are valued at open market price, typically supported by a merchant banker or accountant report.

• Angel tax under Section 56(2)(viib) no longer applies from Assessment Year 2025-26, narrowing the practical use of Rule 11UA(2)’s DCF and VC-benchmarking routes to legacy assessments.

• Rule 11UA remains central to Section 50CA capital gains computations and gift taxation, regardless of the angel tax repeal.

• The Income-tax Act, 2025 carries Rule 11UA’s substance forward, with renumbered cross-references applying from Tax Year 2026-27.

• A defensible, well-documented valuation report reduces dispute risk across share issuances, transfers, gifts and ESOP exercises.

Conclusion

Rule 11UA is not a tax on its own. It is the measuring tape that other provisions use to check whether a transaction involving unquoted shares was priced fairly.

Understanding how that measuring tape works, and which method applies to your specific situation, is the difference between a routine transaction and an unexpected tax notice.

If you’re planning a share issue, transfer, family succession, fundraising round, or any other transaction involving unlisted shares, understanding the applicable valuation requirements before the transaction takes place is far easier than resolving valuation issues later.

At B.B. Mathur & Company, we regularly advise founders, businesses, investors, and family-owned enterprises on share valuation, tax, and regulatory compliance to help them make informed decisions with confidence.

This article is intended for general informational purposes and does not constitute tax or legal advice. Please consult a qualified chartered accountant for guidance specific to your situation.

Sources and References

This guide is based on the following primary sources. Where law has changed, both the original and amended positions are reflected as of the review date above.

- Rule 11UA, Income Tax Rules, 1962, as published by the Income Tax Department, Government of India (incometaxindia.gov.in).

- Income Tax (Twenty-first Amendment) Rules, 2023, notified by the CBDT, effective 25 September 2023, which introduced the current Rule 11UA(2) to (4) structure.

- Finance Act, 2024, which withdrew Section 56(2)(viib) with effect from Assessment Year 2025-26.

- Income-tax Act, 2025 and Income-tax Rules, 2026, effective 1 April 2026.

- Press Information Bureau release on proposed changes to Rule 11UA in respect of angel tax valuation methods.

- Vodafone M-Pesa Ltd. v. PCIT, Bombay High Court (2018).

- Cinestaan Entertainment Pvt. Ltd. v. ITO, Delhi High Court (2021).

- PCIT v. A.H. Multisoft Pvt. Ltd., Delhi High Court (2025)

| Reviewed by Aman Mathur, Partner — Startup Advisory, Valuations & FEMA, B.B. Mathur & Company. Reflects law applicable for FY 2025-26 (AY 2026-27) with notes on the Income-tax Act, 2025 transition |